[ad_1]

Khanchit Khirisutchalual

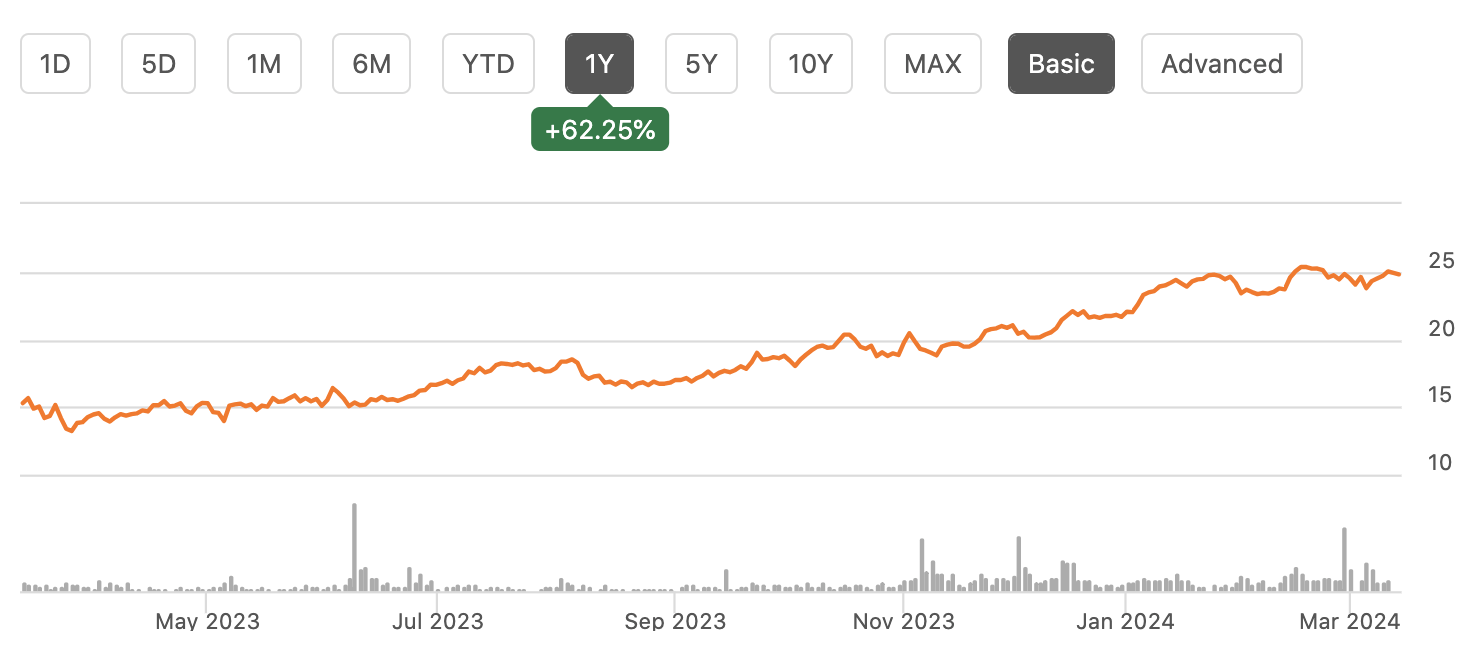

Corebridge Financial (NYSE:CRBG) has been a strong performer over the past year, steadily rising about 62% and now trading near a 52-week-high. The company has performed well with significant capital returns, which has more than offset any headwind from share sales by its former parent, American International Group (AIG). Since recommending shares as a “strong buy” in December, CRBG has returned about 21%, outpacing the S&P 500’s 11% increase. In that piece, I argued shares were worth $28-30, so even with the rally, material upside would remain. Accordingly, with updated financials in hand, now is an opportune time to re-evaluate Corebridge. I remain bullish.

Seeking Alpha

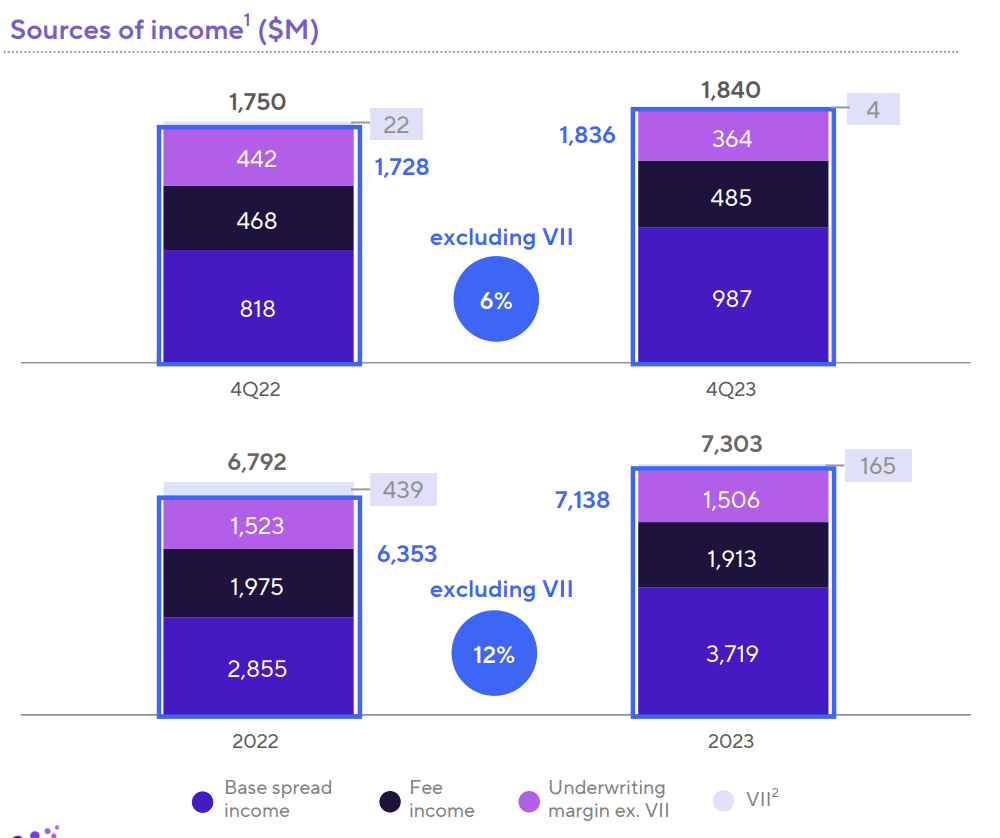

In the company’s fourth quarter reported on February 15, Corebridge generated operating earnings of $1.04, rising 12% from last year. GAAP results were -$2.07 due to movements in derivatives; adjusted EPS beat consensus by $0.18, which is the better measure of the company’s ongoing, run-rate performance. For the full year, operating earnings rose by 12%, expanding its ROE by 90bps as expenses were trimmed by 14%. CRBG generated an adjusted return on equity of 11.2%, up 0.8% from 2022, leaving it well on track to reach its 12-14% target in the coming years.

Corebridge’s income growth is being primarily driven by increased base spread income, with results up about 30% from last year. With elevated yields, CRBG is deploying new funds at the highest interest rate in a decade, increasing its spread income. Additionally, given strength in equity markets, separate accounts returned 10%, increasing the AUM on which Corebridge charges fees. With equity markets remaining robust in 2024, we should see further upside in fee revenue, while the ongoing elevated level of interest rates will continue to be favorable to spread income.

Corebridge Financial

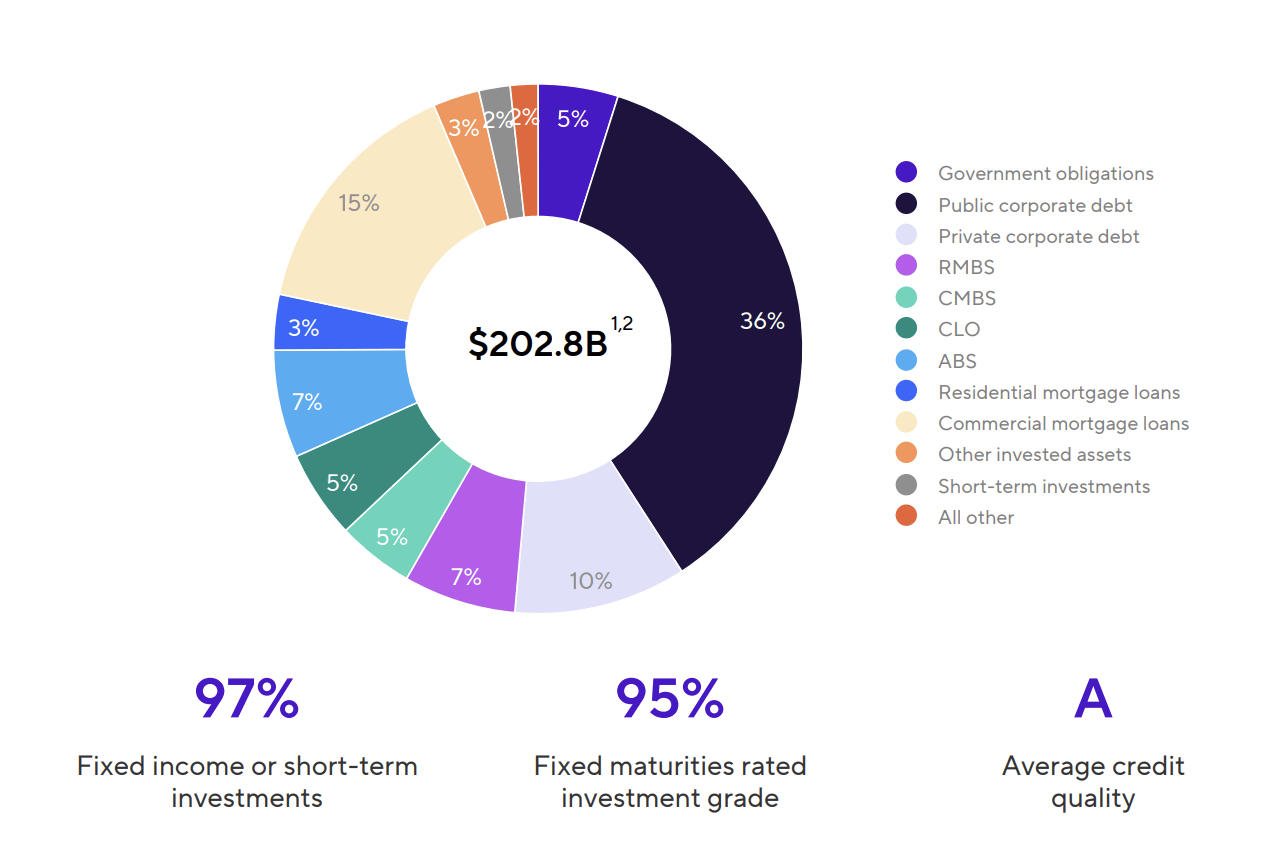

Indeed, CRBG is deploying funds at 7%, increasing the portfolio’s base yield by 17bp sequentially to 4.87%. The company is earning a net of 2.19% on its portfolio, up 2bp sequentially and 23bp from last year. This wider spread alongside portfolio growth has caused net investment income to rise about 15.5% to $2.57 billion. CRBG maintains a fairly high-quality portfolio with a 95% rated investment grade. It does have a 10% exposure to private debt and 5% to collateralized loan obligations, given its outsourced portfolio management to Blackstone (BX). These investments can be less liquid, leading to higher yields. Given its long-dated liabilities, CRBG is rarely, if ever, a forced seller, allowing it to ride through periods of illiquidity and price volatility. They do pose some downside risk if there were to be a recession.

Corebridge Financial

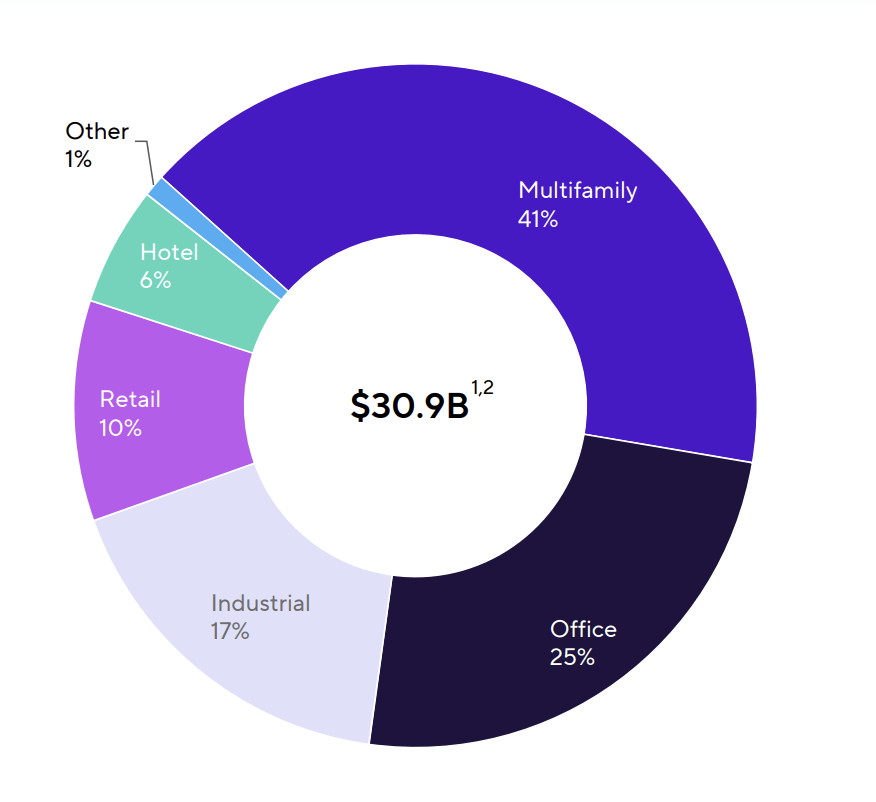

This investment portfolio is somewhat more aggressively positioned than other insurers, but on an absolute basis, it is high quality. CLOs have also proven to be a durable asset class, with top tranches suffering few losses even in the 2008-2009 financial crisis. Moreover, with an economic recession appearing less likely, a large increase in corporate defaults appears unlikely in the near term. Like most insurers and banks, CRBG does have a sizeable commercial real estate position, but I view it as manageable.

This is because its commercial real estate has a 59% average loan-to-value (LTV). Of its $7.6 billion in office, 55% is in traditional office. That is just 2% of the company’s total portfolio. The overall LTV is 63% with 84% occupancy. Importantly, 78% is “Class A,” which has retained better occupancy. Even if we assumed every non-A property defaulted at a 50% loss, that would be a ~$500 million impact pre-tax, realized over several years, given its laddered maturity profile. This is a potential $0.08-0.12 headwind to earnings over the coming years if it plays out. That is quite manageable, and I expect losses to be below this. It does highlight that even if CRE troubles worsen, it is a modest earnings challenge but not a solvency issue.

Corebridge Financial

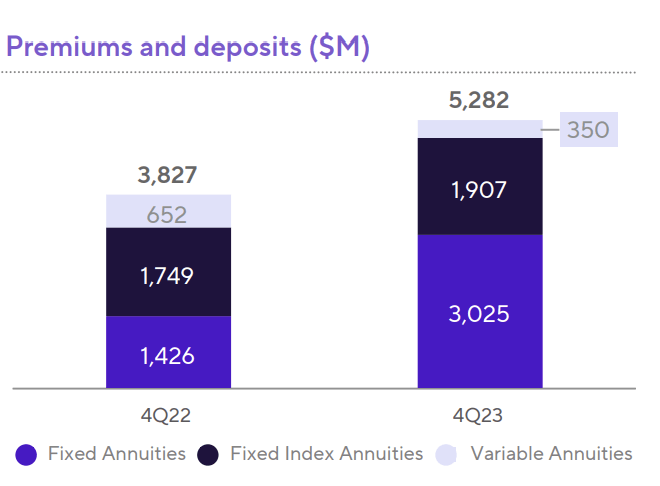

This strong investment income is underpinned by solid results across Corebridge’s units. Individual retirement accounts for about 55% of income. Sales have been very strong with fixed annuities doubling while variable annuities have been nearly cut in half. Fixed annuities are less capital intensive with less complexity than variable annuities, so this mix shift is favorable for Corebridge’s earnings stability. With interest rates rising, there is significantly higher demand for fixed annuities as investors seek to “lock in” these yields, giving CRBG and others the opportunity to boost sales at attractive spread levels (as they pay out lower fixed rates than they invest at).

Indeed, the base investment spread rose to 2.51% from 2.14% last year. While many banks have seen their funding costs (via deposits) rise faster than investment yields, compressing their NIM, CRBG is experiencing the opposite, given its focus further out the curve and increased demand by investors. This is critical because investment spread accounts for about 70% of income. Given wider spreads, operating income rose by 39% from last year to $628 million.

Corebridge Financial

Elsewhere, Group retirement, which accounts for 20% of results, saw income rise a more modest 2% as outflows offset rising fee income. Its institutional markets business, which is increasingly skewed towards pension risk transfers, saw premiums and deposits jump to $2 billion from $1.55 billion. These transactions can be lumpy, given the size of pension deals. It has grown this unit by $7 billion over the past year. Given wider investment spreads, operating income rose by 57% to $93 million. Additionally, having sold its Laya Healthcare until October 31, 2023, it is now in the process of closing the sale of its UK life business. This should free up about $580 million.

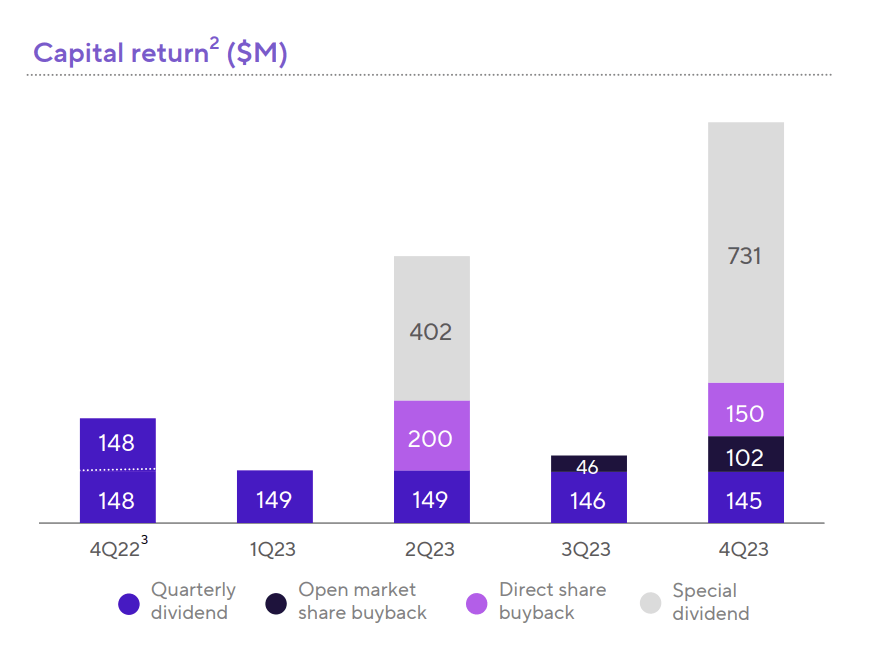

Given these strong results, the insurance company dividend $500 million to the holding company in Q4. The holding company is the entity that repurchases shares and pays the common stock dividend. Importantly, CRBG’s risk-based capital is above the 400% capital adequacy level, which will enable it to continue sending earnings to the parents for buybacks and dividends.

CRBG has been doing this aggressively, with an 84% capital return payout in 2023. Q4 was particularly strong with $1.1 billion of capital returns thanks to a special dividend from the sale of its healthcare unit alongside $252 million of share repurchases. When proceeds from its UK sale are received, I would expect another special dividend beyond its current 4% ordinary dividend yield. Additionally, management is prepared to buy back stock, either in the open market or from AIG. AIG holds about 52% of the company, and I do expect some sales this year. Once it falls below a majority stake, we could see CRBG added to major indices like the S&P 500, and that index-related buying would help offset pressure from further AIG sales.

Corebridge Financial

This is why I believe investors should not let ongoing AIG sales dissuade them from owning CRBG. Indeed, shares have performed very well over the past year despite AIG’s sales. With potential offsetting index purchases, the headwind should be even smaller in 2024. With a recession unlikely, investment results should remain solid. Additionally, this rate environment is favorable for ongoing strength in annuity sales, enhancing the quality of earnings.

With this favorable environment, I believe CRBG is positioned to hit a 12-13% ROE in 2024 from 11.5-12% previously, which will allow $1.4-$1.7 billion in run-rate capital returns to shareholders this year on $4.50-$5.00 in earnings, leaving shares with a 5x multiple and a 10% capital return yield. With book value (excluding unrealized losses) above $37, shares are just 0.7x book value, likely reflecting some legacy variable annuity risk.

I continue to expect shares to march toward $30, or about 0.8x book value, and an 8.5-9% capital return yield, again assuming some discount remains given AIG sales and VA risk. Importantly, with ~$1 billion in share repurchase capacity, AIG can reduce its stake in CRBG by 6% and have this offset by CRBG repurchases, while also further accelerating EPS growth. With this rate environment allowing CRBG to accelerate sales of lower-risk products and boost investment income, there is an ongoing upside, and I would continue to be a buyer, seeing 20-25% total return potential.

[ad_2]

Source link –