[ad_1]

Yves here. Recall that Richard Murphy is a UK commentator, and so his concern about deflation is based on the UK perspective. The last time analysts were concerned about deflation was in the wake of the financial crisis, and there was some discussion of how deflation in the Great Depression made the economic devastation worse. Recall that Irving Fisher’s seminal paper on how debt deflations caused depressions was published in 1933. The critical elements of the dynamic are that deinflation makes it rational to refrain from spending and investment, since things will be cheaper later. That dynamic reinforces contractionary conditions.

The rational place to be as an investor is in cash and extremely safe assets. And borrowers get squeezed since the real cost of their indebtedness rises in deflation. The higher level of defaults amplifies the downdraft.

Moreover, commentators have pointed out that deflation can be exported via lower export prices. That might sound good until you consider that they undercut domestic providers. So what might seem salutary on a small scale can become detrimental.

And in case you think the US is growing too quickly to be at risk, not everyone agrees (hat tip Chuck L):

Another “Blockbuster” Jobs report.

Courtesy of the most creative statisticians government money can buy.

Half the jobs are fake. The other half are government jobs. And there’s been zero new jobs for native-born Americans since… 2018 🤯

How do they get away with it?… pic.twitter.com/5D7PhAbAso

— Peter St Onge, Ph.D. (@profstonge) February 7, 2024

By Richard Murphy, part-time Professor of Accounting Practice at Sheffield University Management School, director of the Corporate Accountability Network, member of Finance for the Future LLP, and director of Tax Research LLP. Originally published at Tax Research

China is suffering deflation, as has been reported this morning:

🇨🇳#inflation #China #reporting

China – consumer inflation CPI (Jan)

m/m = +0.3% (expected +0.4% / previously +0.1%)

y/y = -0.8% (expected -0.5% / previously -0.3%)Traditionally, the media write about deflation in China

The fall in consumer prices in January was the strongest… pic.twitter.com/75KSrAVMSA

— FinNews (@FinNews_) February 8, 2024

In Western economies, like the UK, we have an obsession with inflation because deflation is something that we know almost nothing about as a lived experience. However, we should be worried. Deflation is much more dangerous than inflation and is entirely possible in the UK in the next year or two.

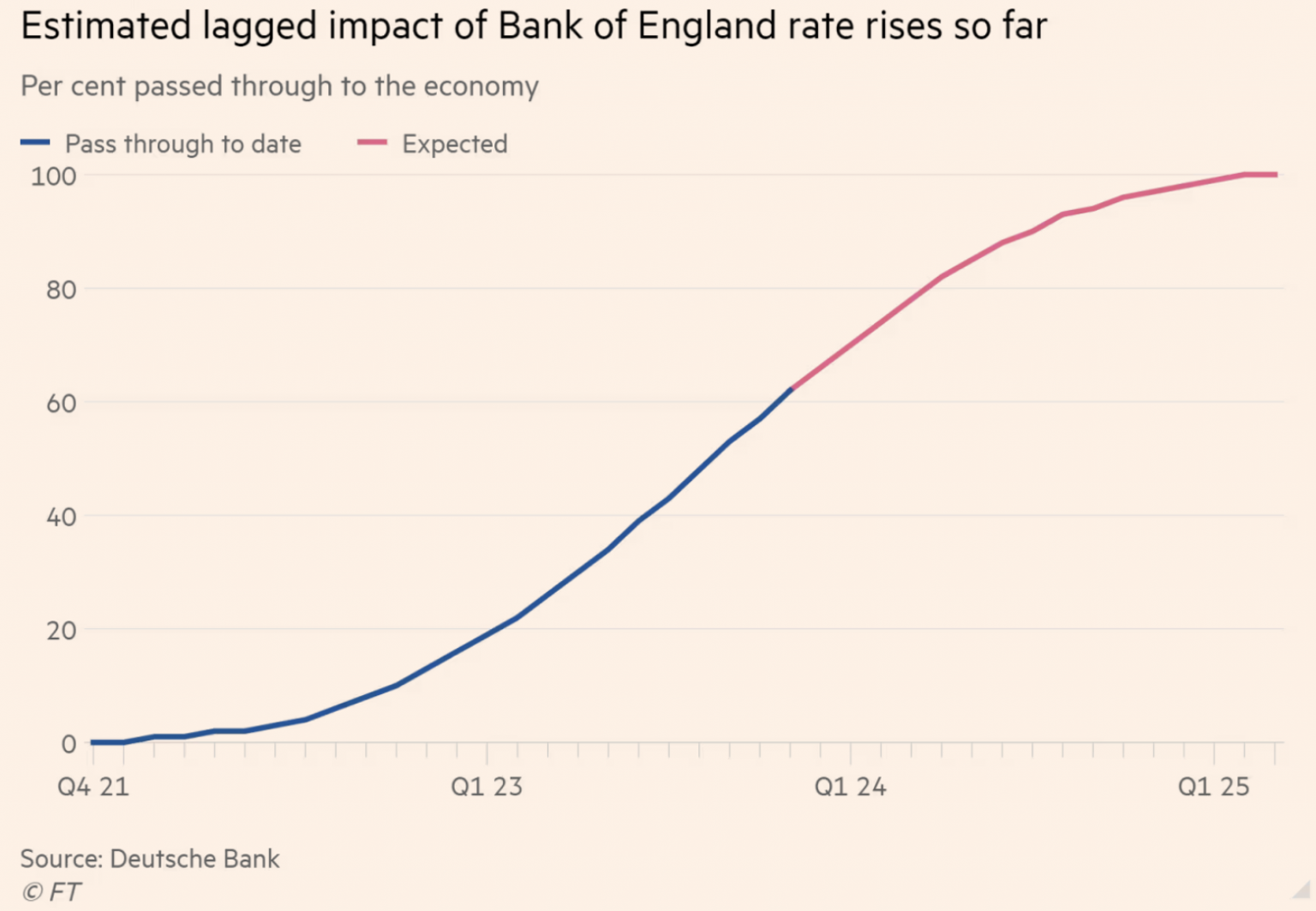

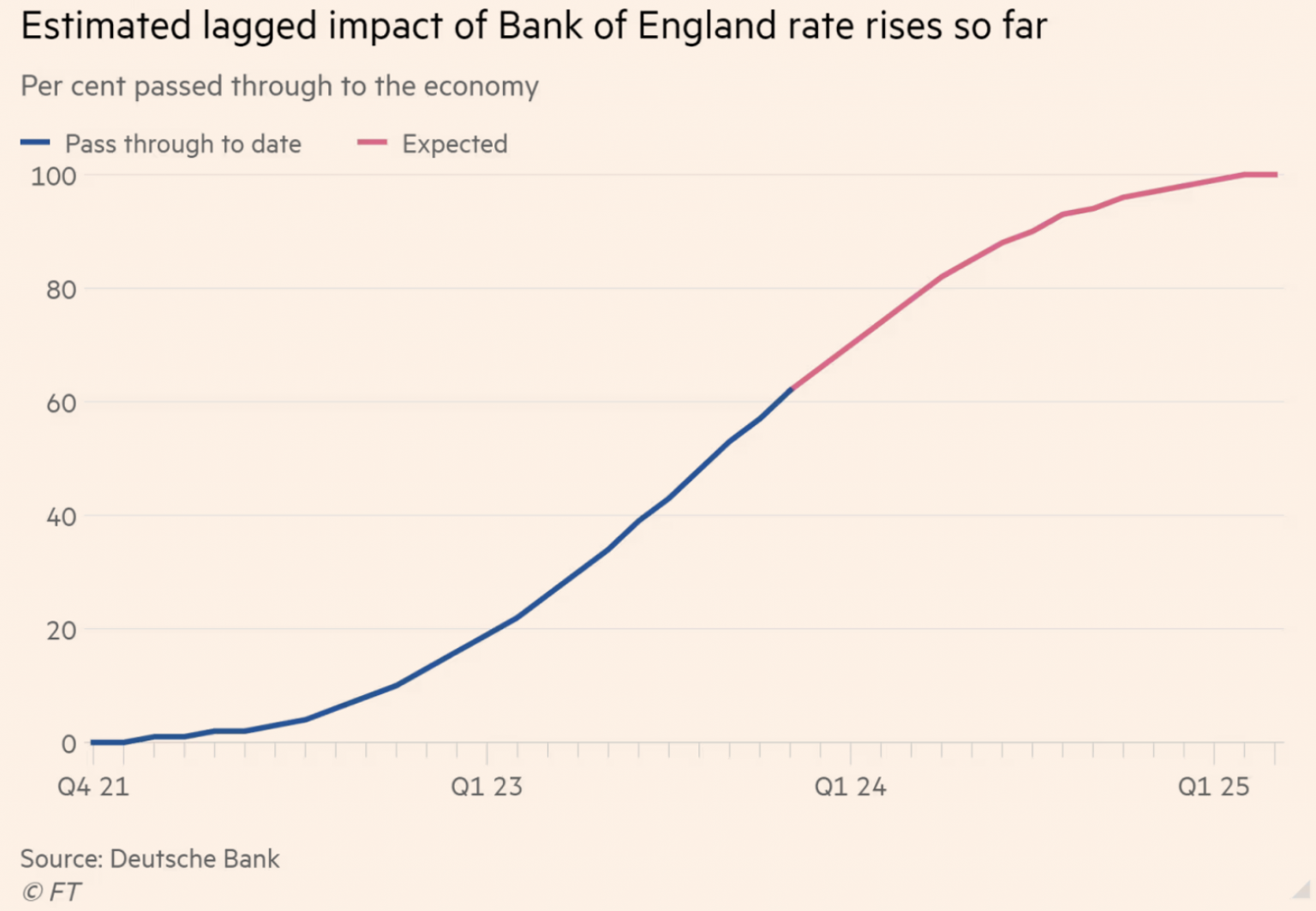

Take a look at this chart, published in the FT this morning that suggests that a significant part of the economic impact of the interest-rate rises put in place by the Bank of England has yet to have an effect, even though we now know that from May this year onwards, inflation in the UK is expected to be less than 3% a year and to remain that way, at best.

High interest rates, which the Bank of England insist must persist, are intended to create a recession by reducing demand, increasing unemployment, and by increasing the cost cost of capital, which cuts the rate of investment. The result is supposed to be significant downward pressure on prices. However, what we know is that those price changes are already falling in scale, significantly. With much of the Bank’s recession-creating effort still to have an impact, the chance that we will have deflation is quite high as a result.

Deflation is dangerous for three reasons.

First, the real cost of repaying loans increases, which penalises all businesses and households that are dependent upon loan finance to make their plans possible. They have to cut their expenditure as a result.

Second, falling prices discourage investment because people defer purchasing decisions in the hope that they can buy things more cheaply in the future.

Thirdly, these two factors do, in combination, put significant pressure on spending capacity, meaning that a steady downward spiral within the economy develops.

As I have long argued, the Bank of England never needed to increase interest rates to tackle inflation because the inflation we had was of a sort that would never have been addressed by interest rate rises and would, in any event, always have passed without any such changes. Now, though, we face the risk of a substantial overshoot by the Bank of England that is very likely to result in a serious recession and potentially in deflation as we follow the path that China is setting.

Economic incompetence of this magnitude takes some effort to deliver.

[ad_2]

Source link –